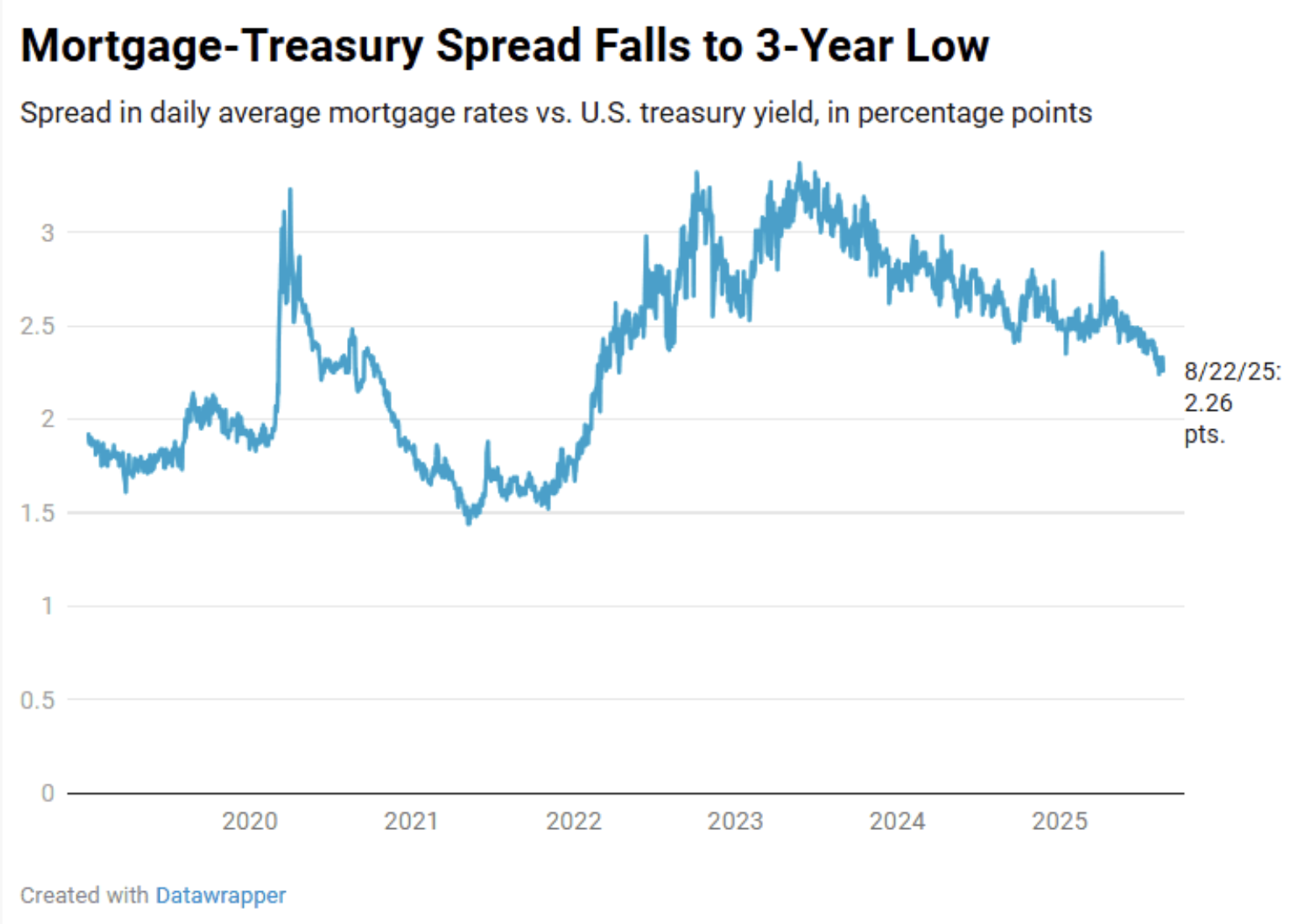

A Brief Primer on Interest Rates

September 5, 2025

September 5, 2025

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Stay up to date on the latest real estate trends.

June 16, 2026

Should I wait for lower interest rates?

May 22, 2026

AI is creating a Bifurcated Market in the K Shaped Economy

December 26, 2025

According to a Zillow analysis, home buying became more affordable in October than it has been in 3 years.

September 5, 2025

How Mortgage Rates Are set

July 15, 2025

Buyers finally gain some levarage

May 10, 2025

You've got questions and we can't wait to answer them.